Sistema Contable ANALITICO-DEPARTAMENTAL (XYZ).

? QUE ES LO QUE SE ENTIENDE POR SISTEMA XYZ ?

En realidad es conseguir una MODELIZACION CONTABLE ANALITICO-DEPARTAMENTAL, sin ampliar sino más bien simplificar el P.G.C. (Plan General Contable), y obtener en, digamos otros planos diferentes los datos ANALITICO-DEPARTAMENTALES.

En el caso de HOTELES, vía la CONTABILIDAD se pueden conseguir además de los informes clásico-financieros de la CONTABILIDAD TRADICIONAL, la CONTABILIDAD ANALITICA, similar y si cabe decirlo más potente todavía, que lo que los americanos han dado en llamar “A UNIFORM SYSTEM OF ACCOUNTS FOR HOTELS” cuya primera edición ha sido publicada en 1.926 por la Asociación de Hoteles de la ciudad de New York.

Actualmente se usa más el concepto USALI (Uniform System of Account for Lodging Industry)

Para ello debemos de tener MUY CLAROS LOS TRES CONCEPTOS SIGUIENTES:

XXX TIPO de INGRESO o GASTO (también llamado ACTIVIDAD)

XXX DEPARTAMENTOS

XX CENTRO de COSTE / HOTEL / RESTAURANTE/ …

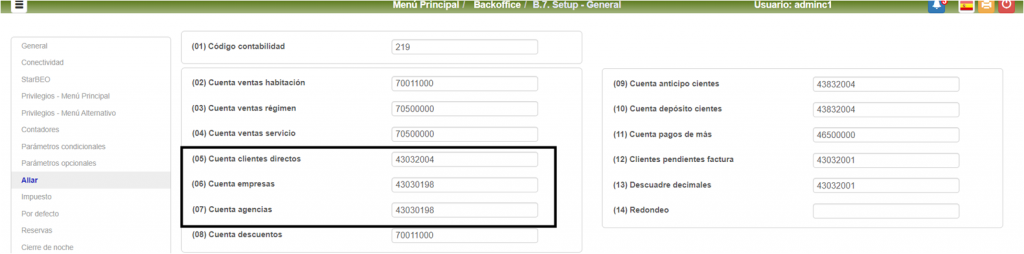

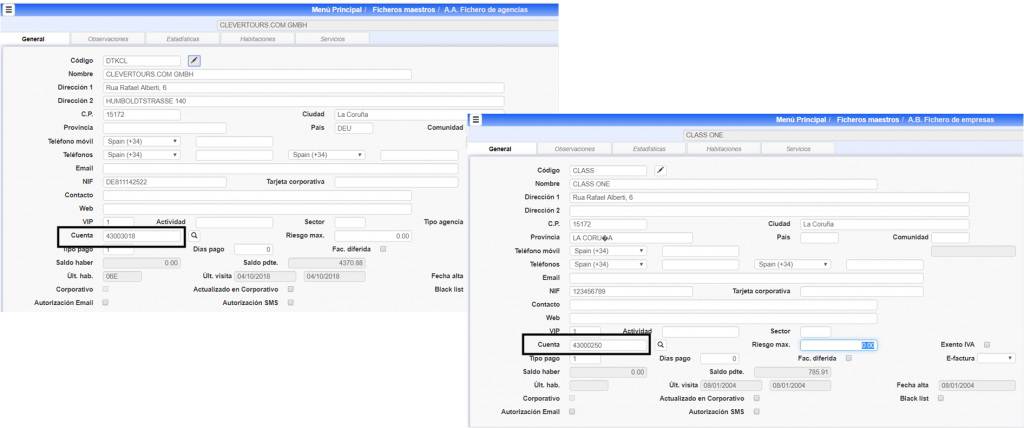

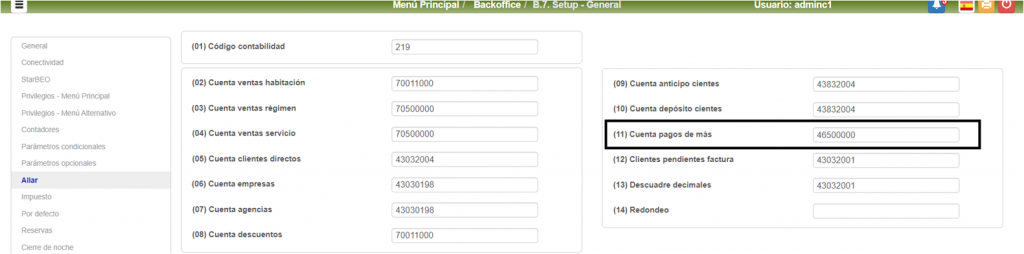

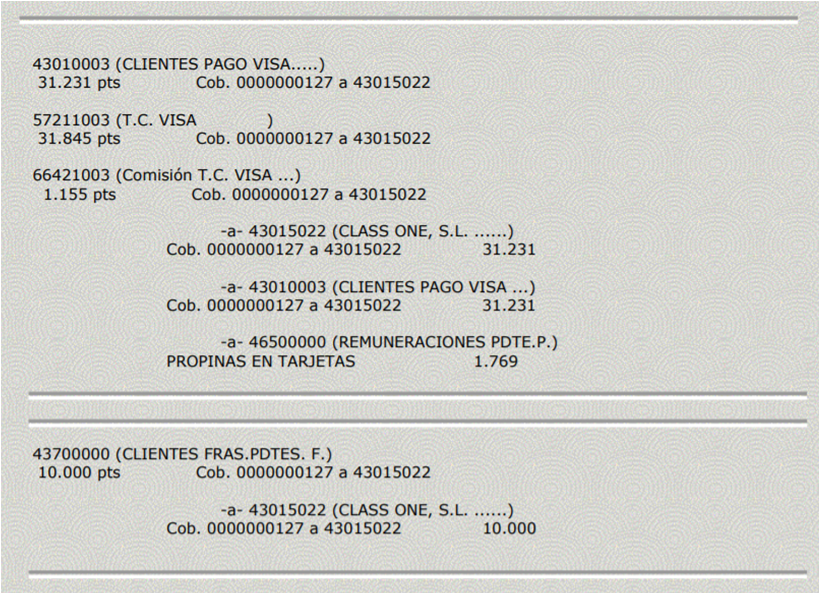

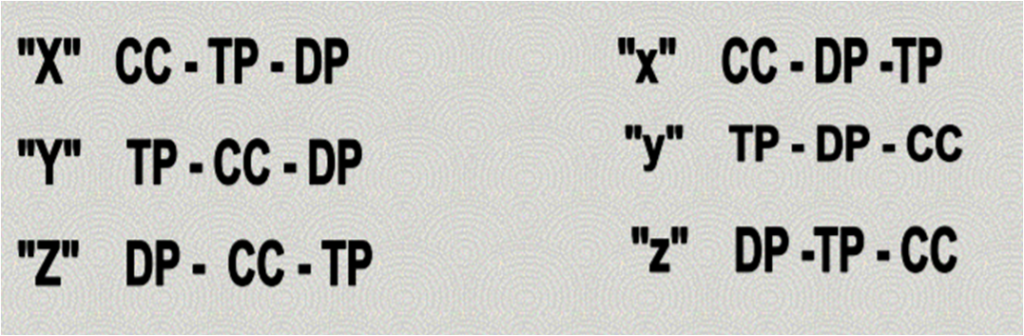

Por ello digamos que dentro de la CONTABILIDAD existe por un lado la CUENTA CONTABLE tradicional del P.G.C., y además otra CUENTA ANALITICA ASOCIADA a cada movimiento “ANALITICO”, formada por:

- xxx. Tipo de INGRESO / GASTO.

- xxx. Departamento ANALITICO.

- xx. Centro de Coste u Hotel.

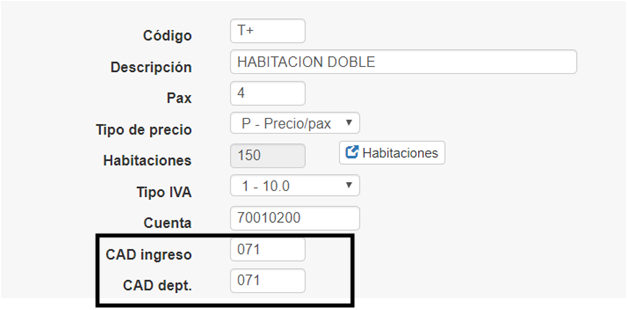

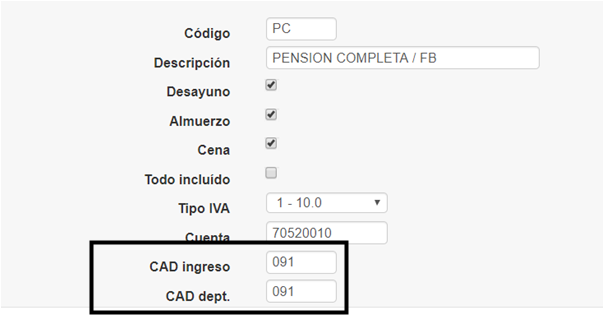

1). TIPOLOGÍA del Movimiento. TIPO de INGRESO o de GASTO.

Significa que debemos de tipificar los movimientos analíticos, mejor llamado ACTIVIDAD en Contabilidad Americana. Veamos dónde y por que.

Concepto sólo INGRESO.

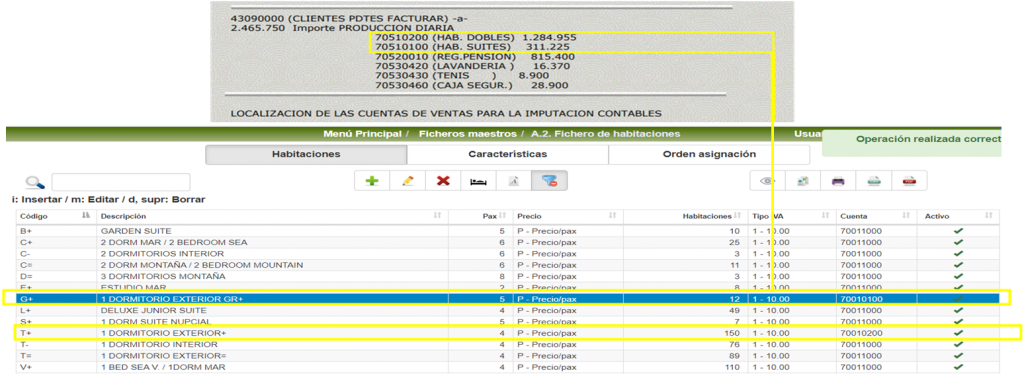

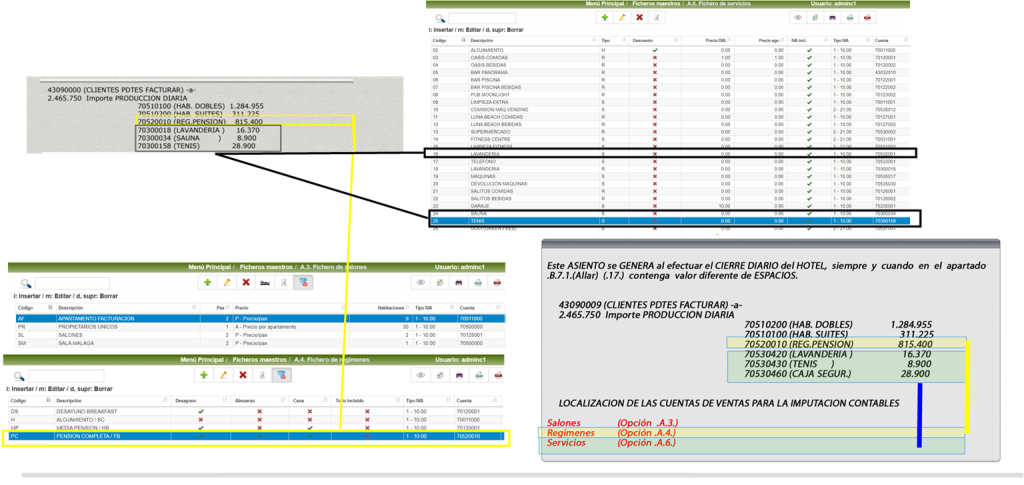

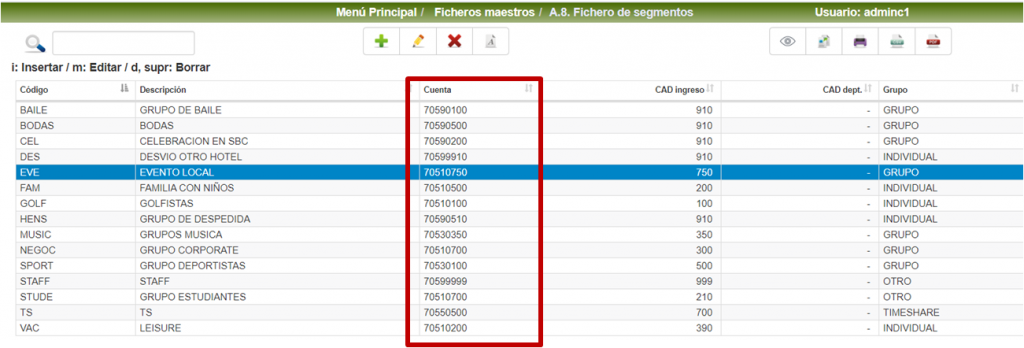

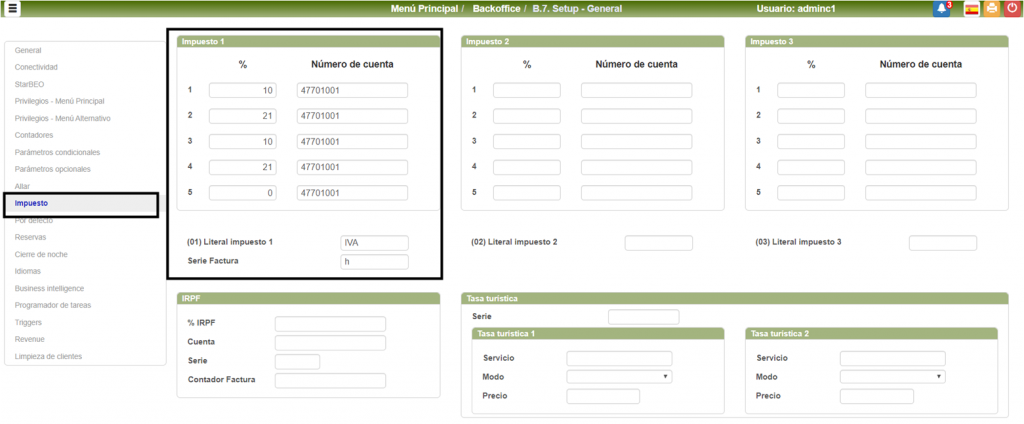

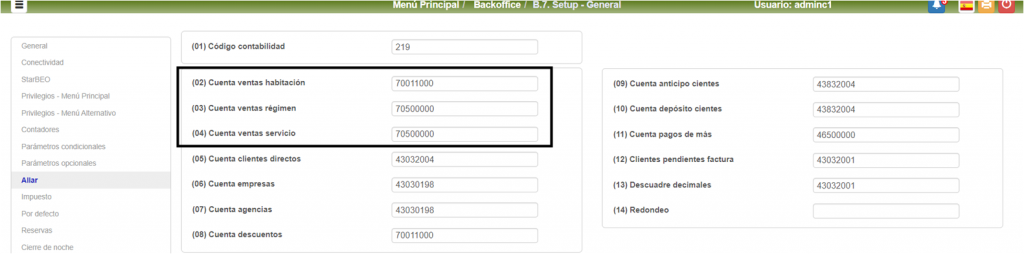

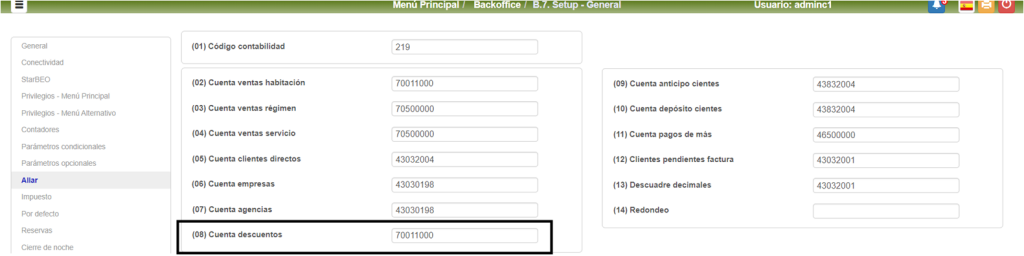

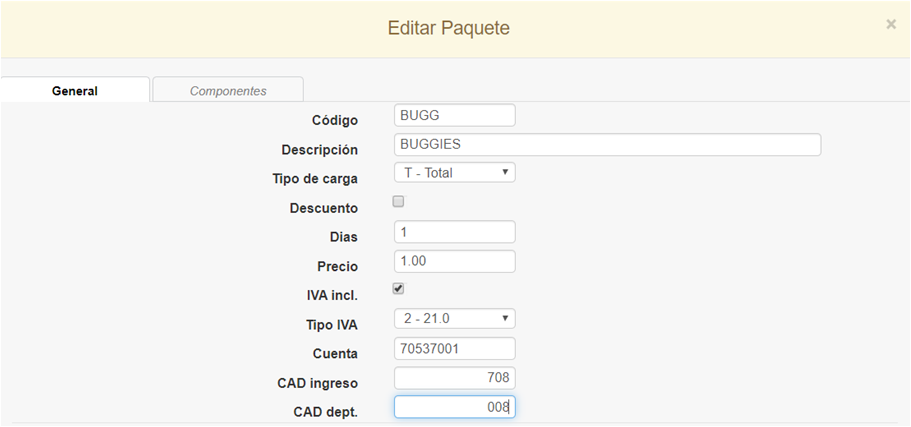

En aquellos conceptos que ya se sabe son exclusivamente de ingresos, se deberá dar un código numérico de 3 posiciones, en nuestro caso afecta a : HABITACIONES, SALONES, REGIMENES, y SERVICIOS.

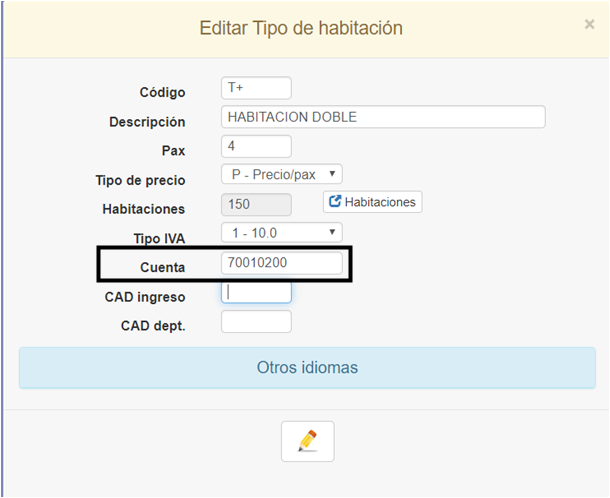

(01). HABITACIONES y/o SALONES. Vemos que en el campo .7. figura tipo de ingreso 071 y como departamento de HABITACIONES y/o SALONES el 071.